Lam Research Corp Stock (LRCX) Moved Up by 4.53% on Apr 24: Drivers Behind the Movement

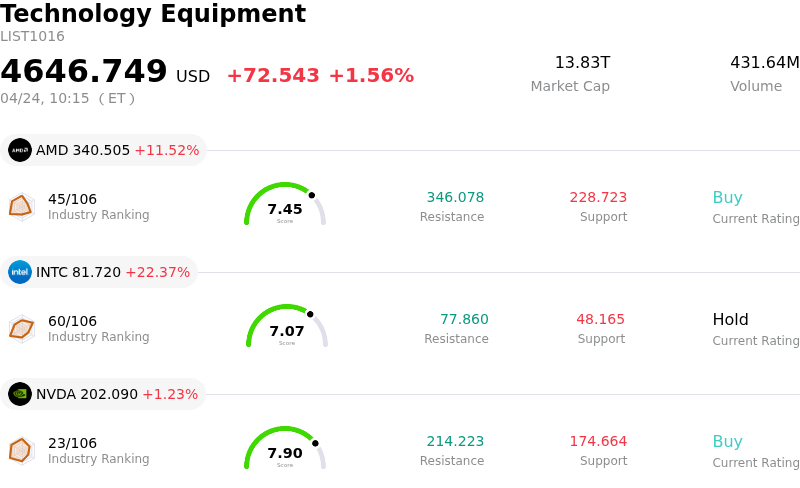

Lam Research Corp (LRCX) moved up by 4.53%. The Technology Equipment sector is up by 1.56%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Advanced Micro Devices Inc (AMD) up 11.52%; Intel Corp (INTC) up 22.37%; NVIDIA Corp (NVDA) up 1.23%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

Lam Research Corporation's stock has experienced positive intraday movement, largely driven by a combination of robust financial performance, optimistic forward guidance, and a favorable industry outlook. The company recently reported its Q1 CY2026 earnings, exceeding analyst expectations for both earnings per share and revenue. Lam Research reported $1.47 earnings per share, surpassing consensus estimates, and revenue of $5.84 billion, also above predictions. This strong performance signals operational efficiency and solid market execution.

Further bolstering investor confidence, the semiconductor equipment manufacturer provided strong guidance for the upcoming Q2 CY2026, projecting revenue and earnings per share well above prior analyst expectations. This upward revision in guidance, coupled with an expansion in operating margins, suggests management's positive outlook on sustained demand within the semiconductor industry. The Customer Support Business Group notably achieved its first quarter with over $2 billion in revenue, highlighting diversified growth.

The broader industry environment is also contributing to the positive sentiment. Lam Research raised its 2026 Wafer Fabrication Equipment (WFE) spending forecast to $140 billion, indicating heightened capital intensity across the sector. This aligns with a general industry trend, as SEMI projects significant double-digit growth in global 300mm fab equipment spending for 2026 and 2027, propelled by surging demand for AI chips in data centers and edge devices. Lam Research management has specifically linked its strong results and guidance to accelerating AI adoption and investments in advanced packaging, NAND, and DRAM technologies.

In response to the positive financial disclosures and market trends, several financial analysts have reiterated "Buy" or "Overweight" ratings for Lam Research and subsequently raised their price targets. Firms such as Royal Bank of Canada, Jefferies Financial Group, JPMorgan, and Goldman Sachs have increased their price objectives, citing the company's strong performance and its central role in the AI-driven chip demand cycle. Strategic developments, including Lam's reported involvement in supporting Tesla's Terafab chip production, also present a potential multi-year revenue stream. Positive earnings reports from industry peers like ASML and ASM International, emphasizing AI-led investment and robust market fundamentals, further reinforce a bullish outlook for the semiconductor equipment sector.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of [9.71], indicating a buy signal. The RSI at 57.19 suggests neutral condition and the Williams %R at -26.21 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $300.46, a high of $385.00, and a low of $196.22.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Lam Research's stock experienced a notable intraday decline on April 23, 2026, despite exceeding Q3 FY2026 earnings and revenue estimates, driven by immediate profit-taking and investor concerns regarding its elevated valuation (high P/E ratio) after a significant prior rally.

- Significant insider selling activity over the past three months, as reported on April 23, 2026, raises potential concerns about management's outlook or signals limited further upside, contributing to negative market sentiment and selling pressure.

- The company's current high valuation and strong market expectations render it particularly susceptible to any future guidance misses or perceived slowdowns in its growth trajectory, creating vulnerability even with positive recent performance.

Nothing in this material constitutes investment advice, personal recommendation, investment research, an offer, or a solicitation to buy or sell any financial instrument. The content has been prepared without consideration of your individual investment objectives, financial situation, or needs, and should not be treated as such.

Past performance is not a reliable indicator of future performance and/or results. Forward-looking scenarios or forecasts are not a guarantee of future performance. Actual results may differ materially from those anticipated.

Mitrade makes no representation or warranty as to the accuracy or completeness of the information provided and accepts no liability for any loss arising from reliance on such information.

Recommended Articles