Lam Research Corp Stock (LRCX) Moved Up by 6.52% on Jun 18: Key Drivers Unveiled

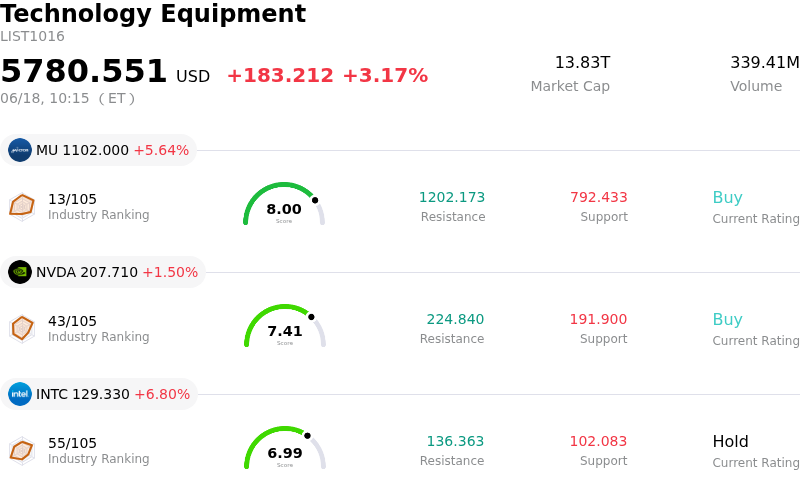

Lam Research Corp (LRCX) moved up by 6.52%. The Technology Equipment sector is up by 3.17%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 5.64%; NVIDIA Corp (NVDA) up 1.50%; Intel Corp (INTC) up 6.80%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

The upward momentum and significant intraday volatility in Lam Research are primarily fueled by a powerful combination of macro tailwinds, surging data center component spending, and a robust outlook for semiconductor capital equipment. A recent market report highlighting triple-digit year-over-year growth in global data center IT spending has re-ignited investor enthusiasm across the semiconductor value chain. Because artificial intelligence infrastructure requires high-density 3D NAND stacks and advanced packaging, Lam Research, as a leading provider of etch and deposition tools, stands out as a primary beneficiary. This demand surge has boosted confidence that the semiconductor capital expenditure cycle is undergoing a prolonged, multi-year expansion.

Crucial to the stock's performance is the company's upgraded global wafer-fabrication equipment market forecast. The company’s management recently indicated that customer demand visibility is the richest it has been in years, driven by the rapid transition to advanced chip architectures. Specifically, the firm's advanced packaging business is emerging as a massive growth driver, with expectations that advanced packaging revenue will grow by more than fifty percent. Since advanced chiplets and high-bandwidth memory depend heavily on deposition-intensive manufacturing processes, investors are treating the business as a highly resilient way to play the ongoing artificial intelligence cycle.

This positive industry outlook is further reinforced by a series of aggressive price target hikes and rating upgrades from major Wall Street institutions. Top-tier financial firms have raised their valuations on the stock, citing booming demand, stronger-than-expected earnings revisions, and a favorable sequential acceleration in revenue. These upgrades have established a strong support level for the stock as analysts increasingly model in sustained memory market recovery and capital spending growth. Additionally, a broader rebound in the technology sector has lifted investor sentiment, encouraging momentum-driven buying.

Despite the strong upward trajectory, the stock continues to exhibit substantial intraday volatility. This is partly driven by market debates over stretched valuations, as some metrics suggest the equity is trading at a premium relative to its historical multiples. Furthermore, underlying option markets have recently recorded unusual trading volumes, reflecting active hedging and contrasting views on short-term price directions. Investors are also closely monitoring potential risks, including high exposure to the Chinese market amid shifting export control dynamics, as well as recent insider selling. However, the overriding structural demand for next-generation semiconductor equipment has dominated the trading session, pushing the stock higher as bulls outweigh short-term valuation concerns.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of 7.671, indicating a buy signal. The RSI at 65.588 suggests neutral condition and the Williams %R at 24.712 suggests buy condition. Please monitor closely.

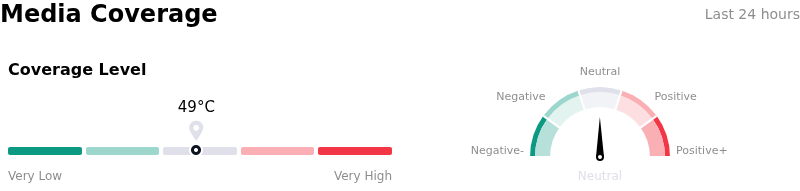

Media Coverage of Lam Research Corp (LRCX)

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $325.89, a high of $420.00, and a low of $213.00.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Projected Shipment Growth Deceleration: Structural concerns have emerged regarding a sharp projected deceleration in system shipment growth, which is expected to plummet to just 3% in 2026 from 82% in 2025 due to cyclical cooling in the NAND memory and China logic markets, threatening near-term top-line revenue expansion.

- Severe Geopolitical and Trade Restrictions in China: With the China market contributing approximately 34% to 35% of overall revenue, Lam is highly vulnerable to expanding U.S. export controls and tool shipment blocks—such as recent restrictions on shipments to China's Hua Hong—which risk permanently impairing its market share in the region.

- Helium Supply Chain Risks for Key Clients: Reports of potential Middle East conflict-driven disruptions to South Korean helium exports threaten to slow down chip fabrication at Lam’s largest customers, Samsung and SK Hynix; because helium is an irreplaceable coolant in fab operations, any shortage would directly curb demand for Lam's etch and deposition tools.

- Insider Divestment Amid Stretched Valuations: A Form 4 filing disclosed that Director Eric Brandt divested 54,500 shares yielding over $19.1 million, which has stoked market anxiety of a near-term valuation peak while the stock trades at a highly stretched trailing P/E exceeding 73x.

Nothing in this material constitutes investment advice, personal recommendation, investment research, an offer, or a solicitation to buy or sell any financial instrument. The content has been prepared without consideration of your individual investment objectives, financial situation, or needs, and should not be treated as such.

Past performance is not a reliable indicator of future performance and/or results. Forward-looking scenarios or forecasts are not a guarantee of future performance. Actual results may differ materially from those anticipated.

Mitrade makes no representation or warranty as to the accuracy or completeness of the information provided and accepts no liability for any loss arising from reliance on such information.

Recommended Articles