Lam Research Corp Stock (LRCX) Moved Up by 4.86% on Jun 17: A Full Analysis

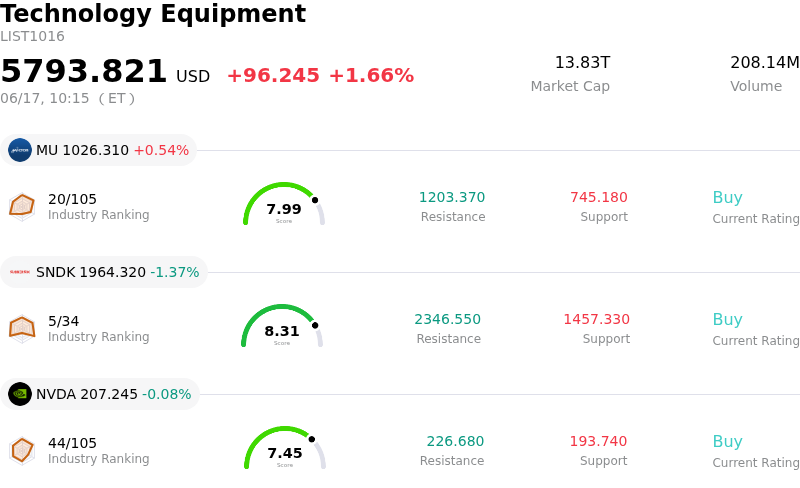

Lam Research Corp (LRCX) moved up by 4.86%. The Technology Equipment sector is up by 1.66%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 0.54%; SanDisk Corporation (SNDK) down 0.74%; NVIDIA Corp (NVDA) down 0.08%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

The upward movement and significant intraday volatility in Lam Research's shares are primarily driven by a confluence of blockbusting industry growth data, favorable analyst updates, and robust fundamentals in the memory semiconductor capital expenditure sector. The primary catalyst for the positive momentum is a newly released industry report indicating a massive surge in global data center component spending, which has directly re-ignited investor enthusiasm for semiconductor equipment manufacturers.

According to the latest market research data released by the Dell'Oro Group, worldwide revenue for Data Center IT Semiconductors and Components experienced triple-digit year-over-year growth in the first quarter of 2026. This growth was heavily propelled by ongoing artificial intelligence infrastructure expansion and rising memory prices, with DRAM contributing the largest share of relative and absolute revenue expansion. Because Lam Research is a dominant leader in supplying the high-aspect-ratio etching and deposition tools required for manufacturing advanced DRAM, 3D NAND, and high-bandwidth memory, the company is directly leveraged to this explosive capital expenditure cycle.

Adding further fuel to the rally, major financial institutions have aggressively upgraded their outlooks for the company. Citi raised its price targets for Lam Research and other wafer-fabrication equipment giants, citing booming demand for NAND equipment and a stronger global spending environment. This positive revision aligns with recent bullish target increases from other major Wall Street firms, including Oppenheimer, Cantor Fitzgerald, and Mizuho, all pointing to AI-driven advanced packaging and memory fab capacity expansion as multi-year growth drivers. This collective optimism is reinforced by the company's upgraded global wafer-fabrication equipment market forecast, which has risen to $140 billion, alongside expectations that its own advanced packaging revenue will grow by over fifty percent in 2026.

This strong microeconomic backdrop helped the stock decouple from broader market headwinds and sector rotation, where high-valuation tech shares saw some profit-taking ahead of the Federal Reserve's latest interest rate decision. The intraday volatility was also likely amplified by the stock trading ex-dividend today for its quarterly payout. While some investors remain cautious about potential export control restrictions and stretched near-term valuations, the recurring high-margin revenue from Lam's massive installed base of over 100,000 active chambers continues to reassure institutional investors of the company’s long-term earnings resilience.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of 8.270, indicating a buy signal. The RSI at 64.563 suggests neutral condition and the Williams %R at 26.270 suggests buy condition. Please monitor closely.

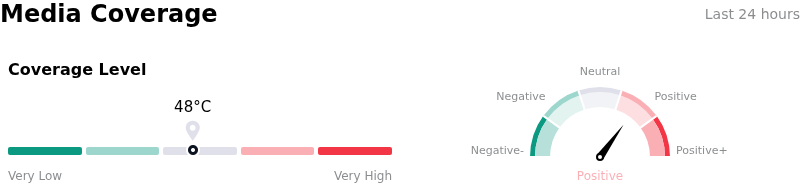

Media Coverage of Lam Research Corp (LRCX)

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 48, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $322.18, a high of $400.00, and a low of $213.00.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- **Extreme Valuation Stretches:** Following a recent 21% surge off its June lows to over $366 per share, LRCX trades at a highly stretched forward P/E of approximately 47x to 50x (and a trailing P/E exceeding 73x, well above its 5-year median of 23x), making it highly susceptible to sudden profit-taking and multiple compression.

- **Drastic Deceleration in System Shipment Growth:** Analysts maintain structural concerns regarding a sharp projected deceleration in system shipment growth down to just 3% in 2026 from 82% in 2025, driven by an expected cyclical cooling of NAND memory and China logic markets.

- **High Geopolitical and Export Control Vulnerability in China:** China accounts for approximately 34% to 35% of Lam’s total revenue, exposing the company to severe top-line volatility and regional market share impairment from expanding U.S. export controls and potential revocations of shipment authorizations.

- **Significant Insider Divestment:** A Form 4 SEC filing on June 15, 2026, disclosed that Director Eric Brandt divested 54,500 shares in multiple open-market transactions, totaling over $19.1 million, fueling market anxieties regarding insider net-selling at a near-term valuation peak.

Nothing in this material constitutes investment advice, personal recommendation, investment research, an offer, or a solicitation to buy or sell any financial instrument. The content has been prepared without consideration of your individual investment objectives, financial situation, or needs, and should not be treated as such.

Past performance is not a reliable indicator of future performance and/or results. Forward-looking scenarios or forecasts are not a guarantee of future performance. Actual results may differ materially from those anticipated.

Mitrade makes no representation or warranty as to the accuracy or completeness of the information provided and accepts no liability for any loss arising from reliance on such information.

Recommended Articles