Dow Jones Hits Record High. AI Tech Theme Recedes, JPMorgan Expects Consumer Staples Stocks to Rebound

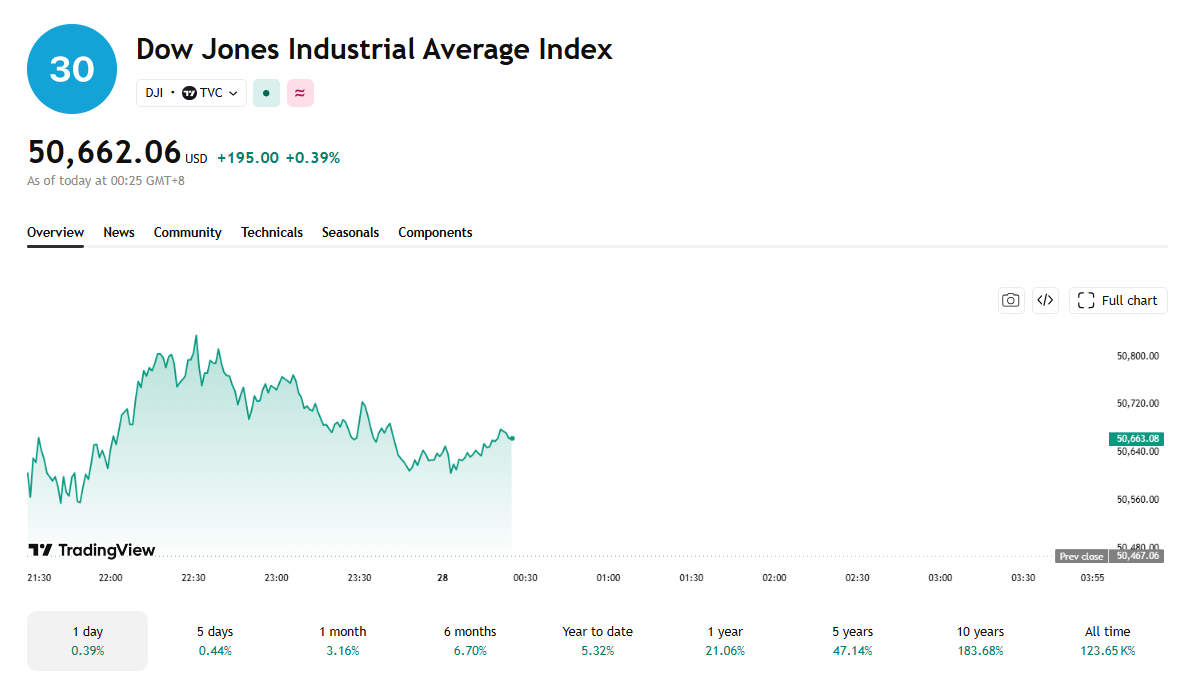

Tradingkey - On May 27, ET, the three major U.S. stock indices showed divergent performance. The Dow Jones Industrial Average hit an intraday all-time high of 50,830.41 points, while the Nasdaq Composite and the S&P 500 turned lower.

U.S. stocks have staged a strong overall rebound over the past two months, but performance disparities among the three major indices are significant. The Nasdaq Composite led the broader market with a cumulative gain of approximately 27%; the S&P 500 rose about 18% over the same period; while the Dow underperformed, gaining only 12% and lagging significantly behind the other two.

[Source: TradingView]

This divergence stems from the distinct structural characteristics of the U.S. stock market. Since the U.S.-Iran conflict entered a stalemate phase, market sentiment has gradually recovered. Earnings expectations for the AI industry continue to improve, serving as the core driver of the market's upward momentum. However, because technology stocks have a lower weighting in the Dow Jones Industrial Average, it failed to fully benefit from this round of tech-driven gains.

Citigroup previously stated that while global earnings per share (EPS) across all sectors are expected to grow in 2026, approximately 50% of that growth is projected to come from the tech sector. This highly concentrated earnings structure is the core logic for a bullish outlook on U.S. equities—the increasing weight of U.S. tech companies in global earnings growth gives the U.S. market a structural advantage in global asset allocation.

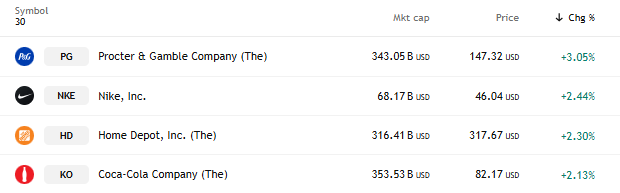

However, looking at today's market divergence, the trend of tech stocks leading the way seems to have shifted: tech stocks fell collectively, while consumer stocks rallied against the trend. Qualcomm ( QCOM) fell 7.56%, leading the decline in the tech sector, while Marvell Technology ( MRVL ), Corning ( GLW ), Intel ( INTC ), Palantir ( PLTR) all followed suit. Meanwhile, previously lackluster performers such as Procter & Gamble ( PG ), Nike ( NKE ), Home Depot ( HD ), Coca-Cola ( KO) collectively strengthened, becoming the day's market highlights.

Looking ahead from the current market juncture, three core variables are collectively influencing the future trajectory of U.S. stocks: a ceasefire agreement between the U.S. and Iran, the upcoming first FOMC meeting under new Fed Chair Kevin Warsh, and the market's pricing in of a new Fed rate hike cycle.

Against this backdrop, whether the Dow Jones Industrial Average—which has recently underperformed the Nasdaq and S&P 500—can reclaim its role as the primary market theme has become a key focus for investors.

JPMorgan Chase released an analysis of market conditions, stating that the market is currently significantly overestimating the probability of interest rate hikes by major global central banks. This mispricing has created a clear window for a rebound in low-volatility defensive stocks, such as consumer staples and utilities.

The firm added that while investors generally worry that energy price shocks from the Iran conflict could trigger a new rate hike cycle similar to the one following the 2022 Russia-Ukraine conflict, it believes the current geopolitical environment is fundamentally different from that of 2022.

The report noted that the ultimate goal for all parties in this conflict remains seeking a peaceful solution; therefore, global bond yields and international oil prices are expected to fall below current levels over the next 6 to 12 months.

Throughout this AI-driven bull market, low-volatility stocks have been largely overlooked. A Goldman Sachs indicator measuring 'U.S. cyclical stocks' performance relative to defensive stocks' has reached an 18-year extreme.

JPMorgan noted that the significant correction in low-volatility stocks in the U.S. and Europe over the past few months, as bond yields rose, has instead highlighted their allocation value. Besides consumer staples and utilities, insurance stocks and certain industrial stocks share similar characteristics. These stocks offer value regardless of the future direction of U.S. Treasury yields.

The firm continued that if the 10-year Treasury yield surges toward the 5% mark, low-volatility stocks could break their traditional inverse correlation with interest rates and outperform due to being oversold. Conversely, if the rise in bond yields subsides, low-volatility stocks are expected to return to the outperformance seen before the outbreak of the Iran conflict.

Nothing in this material constitutes investment advice, personal recommendation, investment research, an offer, or a solicitation to buy or sell any financial instrument. The content has been prepared without consideration of your individual investment objectives, financial situation, or needs, and should not be treated as such.

Past performance is not a reliable indicator of future performance and/or results. Forward-looking scenarios or forecasts are not a guarantee of future performance. Actual results may differ materially from those anticipated.

Mitrade makes no representation or warranty as to the accuracy or completeness of the information provided and accepts no liability for any loss arising from reliance on such information.

Recommended Articles