TradingKey’s The Week on Wall Street: "Super Central Bank Week" Arrives,Fed Decision and Warsh Debut Lead, Markets Eye US-Iran Talks

Previous Week’s Market Review & Analysis

TradingKey - The US Consumer Price Index (CPI) for May, released on June 10, showed an acceleration to 4.2% overall inflation and 2.9% core inflation. The Producer Price Index (PPI) for May, released on June 11, increased 1.1% monthly and 6.5% annually, with core PPI up 0.4% monthly and 4.9% annually. Initial Unemployment Insurance Claims rose to 229,000, signaling a slight increase in joblessness. Geopolitical tensions related to the US-Iran conflict persisted, contributing to renewed inflation fears and potential impacts on oil prices. The Federal Reserve's target range for interest rates remained at 3.50% to 3.75%.

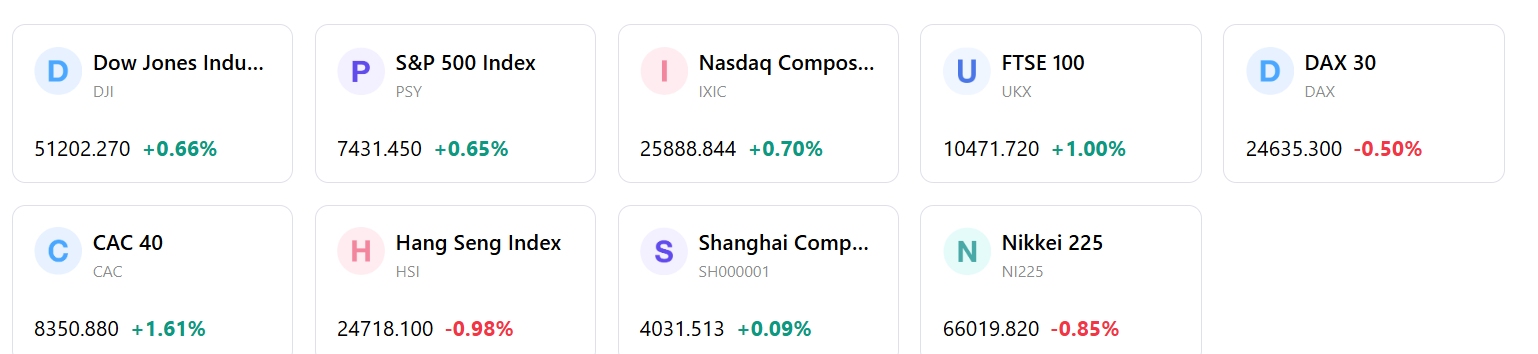

Market Performance Overview: US equity markets started the week of June 8 with mixed results; the Nasdaq recovered some losses, and the S&P 500 saw modest gains, while the Dow was little changed and the Russell 2000 finished positively. On June 8, the S&P 500 rose 0.30% to 7,405.73, with technology and growth stocks leading the gains. However, on June 10, U.S. stocks declined, with the Dow Jones falling 1.87% to 49,918.78, and both the S&P 500 and Nasdaq also decreasing; the Nasdaq was down approximately 7% from its June 1 peak. By June 12, risk assets had stabilized and closed higher across the board. The S&P 500 rose 0.61%, the Dow Jones Industrial Average rose 0.65%, the Nasdaq Composite rose 0.70%, and the Russell 2000 rose 0.8%.

Key Events Analysis: The US Consumer Price Index (CPI) was released on June 10. The Producer Price Index (PPI) and Initial Jobless Claims were released on June 11. Oracle reported strong Q4 earnings during the week, although its shares dropped following a financing plan. Adobe's earnings were also anticipated on June 11. Geopolitical tensions concerning the US-Iran conflict continued to be a market factor.

Flows & Sentiment: Investor sentiment for technology and AI-related stocks, strong earlier in the month, was curtailed by concerns over Fed policy and inflation. The VIX volatility index was recorded at 21.51 on June 5, indicating underlying market uncertainty. The Nasdaq experienced persistent outflows since June 5, attributed to a combination of the "AI credit cycle" and "geopolitical inflation cycle".

Overall Assessment: The market exhibited a dual character this week, initially influenced by strong corporate earnings and hopes for easing geopolitical tensions, but subsequently affected by inflation concerns and Federal Reserve policy expectations. The period was marked by significant market sensitivity to macroeconomic data and the monetary policy outlook. Strong jobs data from the prior week (June 5) heightened expectations for a more aggressive Federal Reserve, contributing to a sell-off in growth and technology sectors at the beginning of the June 8-14 week. The market is navigating a complex environment characterized by high interest rates, trade tariff policy, and elevated energy prices.

Next Week's Key Market Drivers & Investment

Upcoming Events: The Federal Open Market Committee (FOMC) will hold a meeting on June 16-17, including a rate decision and press conference by the new Fed Chair, Kevin Warsh. The Summary of Economic Projections, also known as the dot plot, will also be released during this meeting. Key economic data releases will include US Industrial Production for May on June 15, and US Retail Sales on June 17. Central bank decisions are anticipated from the Bank of Canada, European Central Bank, Bank of Japan, RBA, SNB, and Bank of England. Notable companies scheduled to report earnings include Jabil, Accenture, FedEx, and Micron Technology.

Market Logic Projection: Market logic will likely be heavily influenced by the FOMC meeting, particularly the statements from Fed Chair Warsh and the Summary of Economic Projections, which will shape expectations for Federal Reserve policy. Geopolitical tensions are expected to remain a factor, potentially impacting oil prices and market volatility.

Strategy & Allocation Recommendations: Investors are advised to maintain exposure to quality growth stocks, particularly within technology and AI themes, despite recent market fluctuations.

Risk Alerts: Key risks include ongoing inflation concerns, persistent geopolitical influences, and narrow market leadership. The Federal Reserve's communication during the upcoming FOMC meeting is particularly consequential, with the potential to introduce significant market volatility.

Markets Weekly

5-Day Index Performance

Nothing in this material constitutes investment advice, personal recommendation, investment research, an offer, or a solicitation to buy or sell any financial instrument. The content has been prepared without consideration of your individual investment objectives, financial situation, or needs, and should not be treated as such.

Past performance is not a reliable indicator of future performance and/or results. Forward-looking scenarios or forecasts are not a guarantee of future performance. Actual results may differ materially from those anticipated.

Mitrade makes no representation or warranty as to the accuracy or completeness of the information provided and accepts no liability for any loss arising from reliance on such information.

Recommended Articles